Opening your mailbox to find a letter from the IRS is never a "good news" situation. But in 2026, with the IRS ramping up its automated collection systems, the letters are coming faster, and the language is getting tougher. If you’ve received a CP504 or an LT11, you aren’t just looking at a bill; you’re looking at a countdown.

The biggest question I get at Wolf Tax is: "Are they actually going to take my money today?"

The answer depends entirely on which code is in the top right corner of that envelope. While both notices address a tax levy, they represent two very different stages of the IRS collection process. One is a warning shot; the other is the IRS reaching for your wallet.

In this guide, I’m going to break down the technical differences, the strategic risks, and the "Golden Rules" for surviving these notices without losing your shirt.

The CP504 Notice: The IRS "Shot Across the Bow"

If you just received a CP504 (Notice of Intent to Levy), take a deep breath. You are in the "Urgent but Not Quite Desperate" phase.

The CP504 is generally the penultimate warning in the IRS collection cycle. Its primary purpose is to inform you that you have an unpaid balance and that the IRS intends to seize property or rights to property if you don't pay up within 30 days.

What the IRS Can Actually Do With a CP504

Here is the strategic reality: Despite the scary language, the CP504 has limited "teeth" compared to what comes next.

- The State Refund Trap: The most immediate power the CP504 gives the IRS is the right to seize your state income tax refund. They don't need another warning for this. If you owe Uncle Sam and you were expecting a check from the state, consider that money gone.

- The Search for Assets: This notice signals that the IRS is now actively looking for your bank accounts, your employer’s payroll department, and any other assets they can find.

- The "Soft" Levy: While they can begin looking at other assets, they usually use the CP504 as a final "nudge" before they pull out the heavy artillery.

The Winner in This Scenario: You, but only if you act now. At the CP504 stage, you still have time to set up a tax resolution plan before the IRS starts freezing your bank accounts.

The LT11 (and Letter 1058): The "Red Alert" Notice

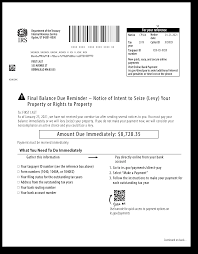

If you see LT11 (or its cousins, the CP90 or Letter 1058) on your desk, the situation has escalated. This is officially the Final Notice of Intent to Levy and Notice of Your Right to a Hearing.

This is not a drill. This is the IRS telling you that the 30-day clock has started, and once it hits zero, they have the full legal authority to:

- Garnish your wages: They will contact your boss, and a huge chunk of your paycheck will go directly to the IRS before you ever see it.

- Freeze your bank accounts: They will send a notice to your bank. Your funds will be frozen for 21 days, and if the issue isn't resolved, the bank will send that money to the IRS.

- Seize property: This includes vehicles, real estate, and business equipment.

- Federal Tax Liens: They will likely file a tax lien, which attaches to everything you own and can wreck your credit and ability to sell property.

The Most Important Part of the LT11: Your Due Process Rights

The LT11 is scary, but it actually gives you a "secret weapon" that the CP504 does not: The Collection Due Process (CDP) Hearing right.

Because the LT11 is a "Final Notice," the law requires the IRS to give you a chance to argue your case before an independent Office of Appeals. If you file Form 12153 within the 30-day window, you can effectively "freeze" the IRS collection actions.

The Strategic Play: If you miss the 30-day deadline on an LT11, you lose your right to go to Tax Court. This is the single biggest mistake taxpayers make. They wait until day 31, and by then, the IRS is already dialing their bank.

CP504 vs. LT11: The Core Differences at a Glance

To make this easier to scan, here is how these two notices stack up against each other:

| Feature | CP504 Notice | LT11/Letter1058 |

| Stage | Preliminary Warning | Final Warning |

| State Refund Seizure | Yes, immediate after 30 days | yes |

| Bank Account Levy | Possible, but rare immediately | Primary Goal |

| Wage Garnishment | Possible, but rare immediately | Primary Goal |

| CDP Hearing Rights | No | Yes (Crucial) |

| Tax Court Access | No | Yes (if timely filed) |

| Urgency Level | High | Critical |

The "Collection Clock": How the IRS Moves

Understanding the IRS’s motivations is key to staying calm. They don't want to seize your house; it’s a lot of paperwork. They want the easiest path to the money.

- If you receive a CP504: You are likely 30–60 days away from a total financial lockdown. The IRS is currently "cleaning up" its files and getting ready to send the Final Notice.

- If you receive an LT11: You are 30 days away from a tax levy.

In 2026, the IRS is using advanced data matching to find your assets faster than ever. If you changed jobs or opened a new bank account six months ago, don't assume they don't know. They do.

Strategic Decisions: What Should You Do Next?

When you’re staring at these notices, you have three main paths. Choosing the right one is the difference between financial recovery and a total "anchor" on your future.

1. The "Fresh Start" Play

If you owe a significant amount but don't have the assets to pay it, you might qualify for an IRS Offer in Compromise. This allows you to settle your debt for less than you owe. However, filing for an OIC requires precision. If you do it wrong while an LT11 is active, you might accidentally give the IRS more time to collect later.

2. The "Currently Not Collectible" Play

If paying the IRS would leave you unable to pay basic living expenses (rent, food, utilities), we can often get you placed in Currently Not Collectible status. This stops all levies and garnishments while you get back on your feet.

3. The Installment Agreement

Sometimes, the smarter play is simply to negotiate a payment plan that fits your budget. This stops the "collection clock" and keeps the LT11 from turning into an actual bank seizure.

Why You Shouldn't Handle This Alone

The IRS is a bureaucracy, not a person. When you call them yourself, you are speaking to an agent whose job is to secure payment. They aren't there to tell you about the IRS Fresh Start Program or explain how to use your First Time Abate rights.

At Wolf Tax, we step between you and the IRS. When we take over, we handle all the communication.

- We file the Stay of Collection.

- We request the CDP Hearing.

- We analyze your financial "RCP" (Reasonable Collection Potential) to see if we can get your debt reduced.

Expert Analysis: The IRS often sends a CP504 after a series of other letters you might have missed (CP14, CP501, CP503). If you are seeing a CP504 for the first time, your "CSED" (Collection Statute Expiration Date): the 10-year limit the IRS has to collect: might be closer than you think. We check these dates to see if we can simply wait out the clock.

The "Golden Rules" of IRS Notices

- Never ignore an LT11. It is the legal "trigger" for asset seizure. If you ignore it, you lose your right to appeal in court.

- Verify the amount. The IRS is frequently wrong. We often find that penalties can be removed using penalty abatement strategies, significantly lowering the total bill.

- Don't wait for the levy to happen. It is 10x harder to get money back from the IRS than it is to stop them from taking it in the first place.

Summary: Is Your Money Safe?

If you have a CP504, your bank account is likely safe for the next few weeks, but your state refund is at risk.

If you have an LT11, your money is in immediate danger. You have exactly 30 days from the date on that letter to file a protest and protect your assets.

Don't let the stress of these notices paralyze you. The IRS is predictable, and they have rules they must follow. At Wolf Tax, we know those rules better than anyone. Whether you're in Detroit or anywhere else across the country, we can help you navigate the tax resolution process and get the IRS off your back for good.

Ready to stop the clock? Contact Wolf Tax today and let us deal with the IRS so you don’t have to.

Help! I Just Received an IRS Notice of Intent to Levy (CP504)

IRS Letter in the Mail? Here’s Exactly How to Stop a Tax Levy Before Your Next Paycheck